Facts You Need to Know About SB553

SB553 - Requiring taxpayer funds held by the Public Deposit Investment Pool (PDIP) be insured or collateralized and kept within New Hampshire

- Are Taxpayer Dollars in PDIP Insured or Collateralized?

Taxpayer funds in PDIP are NOT insured by the Federal Deposit Insurance Corporation or any other government agency or secured through collateralization despite this being a common practice by banks. - Are Taxpayer Dollars in PDIP working for the Granite State Economy?

The taxpayer funds held by PDIP DO NOT remain within the state and are NOT put to work for New Hampshire's economy. At the Senate Finance hearing on SB 553 held on January 30, 2024, PFM Representatives who manage PDIP funds, testified that ZERO dollars [at 44:07] from the pool remain in New Hampshire.

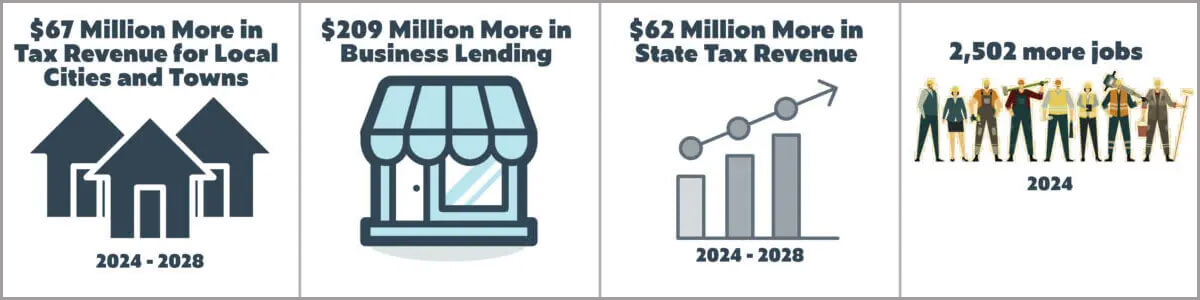

The economic firm Polecon conducted a study on what would happen to our State's economy if those funds stayed in the Granite State. Here's what was found. (Data updated April 2024)

- If funds were kept in NH in 2023, it would have increased the state's GDP by nearly $221 million.

- Conservatively projects an additional $209 million available for NH business lending, primarily benefitting small businesses with fewer than 50 employees

- Projects an increase of $67 million in local tax and fee revenues and $62 million in state revenue over the next five years.

- Interest from bank deposits in New Hampshire, coupled with boosted tax revenues from business lending and state GDP growth, could reach $58.4 million annually at a 10.35% yield.

- Projects personal income to increase by as much as $226 million.

Recent articles about SB553 in New Hampshire.

Opinion: NH should support SB 553 - Concord Monitor 5/7/24

Sen. Rosenwald: Let's put New Hampshire Funds to Work in New Hampshire - Seacoastonline 4/16/24

Strengthen our Economy by Leveling the Playing Field for NH Banks - Union Leader 4/12/24

Public Investment - InDepthNH 2/21/24

Stashing the Cash at Home - Business NH 1/5/24

SB553 - Questions and Answers

At the public hearing on SB553 in the Senate Finance Committee, the State Treasurer testified that the State is receiving a rate as high as 5.25% from a bank in New Hampshire. Watch the video: [at 1:26:10]

See a five-year rate comparison and hypothetical examples of rates received by a town depositing taxpayer funds in a Bank versus PDIP.

Furthermore, the study demonstrates that funds kept in State provide an exponentially higher total economic impact and return, regardless of the specific deposit rate.

Lastly, not every state has a pool similar to NH PDIP. The closest examples of these are Vermont and Maine. Despite not having a local government investment pool, they have a competitive environment benefitting municipalities and taxpayers.

Banks - Public funds held by banks are insured by the FDIC up to $250,000. Insurance is available at higher levels through different products. Through FDIC insurance taxpayer funds are backed by the full faith and credit of the U.S. Government. In addition to insuring the funds, banks can offer additional collateralization.

PDIP - Many states have similar type pools however, they do carry risk. The NH PDIP displays a disclaimer that funds are not insured by any government institution and acknowledge the risk of loss.

Additionally, according to the S&P Global pool profile of NH PDIP, "Generally, when faced with an unanticipated level of redemption requests during periods of high market stress, the manager of any fund may suspend redemptions for up to five business days or meet redemption requests with payments in-kind in lieu of cash."

Ratings Misnomer - Ratings are only required for debt issuances that are widely traded and where the risk of loss is present. Community banks generally do not issue these types of debt securities; therefore, most are not rated at all.

In accordance with state law, banks are required to offer collateralization above the FDIC-insured limit of $250,000, resulting in zero risk of loss regardless of the bank they are held in. Debt ratings aren't relevant or required.

PDIP focuses on debt/credit ratings because it is putting hundreds of millions of dollars that belong to New Hampshire taxpayers at risk with no insurance or collateral of any kind as a backstop. All of the money in PDIP - money that was earned and paid in taxes by hardworking citizens of New Hampshire - could be lost. It is not insured, collateralized or guaranteed in any way.

Currently, there are ZERO dollars from the over $600 million invested with PDIP re-invested in New Hampshire. These are New Hampshire taxpayer dollars leaving the state.

Here are 3 examples: To see the full list of investments click here.

- National Australia Bank

- Skandinaviska Enskilda Banken

- Sumitomo Mitsui Bank

If a municipality or public entity wants access to their funds from a bank, those funds are immediately available. If funds are placed in a timed deposit like a certificate of deposit (CD), there may be a penalty if funds are withdrawn prematurely, but the funds are always available if needed.

This is not the case for PDIP. According to the S&P Global the fund manager of PDIP however, in periods of high stress can place a pause on redemptions for up to five business days or "meet redemption requests with payments in-kind in lieu of cash."

Public funds held by banks are insured by the FDIC up to $250,000. Insurance is available at higher levels through different products such as ICS or Intrafi. Through FDIC insurance taxpayer funds are backed by the full faith and credit of the U.S. Government. In addition to insuring the funds, banks can offer additional collateralization through a repurchase agreement with the Federal Reserve, a letter of credit from the Federal Home Loan Bank or pledging of other high quality securities and assets.

No. Today, the state, cities, towns and managers of public funds have a wide range of options to manage taxpayer funds in a manner of their choosing as laid out throughout New Hampshire statutes. They can invest funds in PDIP, or outside of PDIP, directly with a financial institution, or through a broker, so long as the management of taxpayer funds are consistent with their applicable investment policy.

If SB 553 passes, public fund managers are still able to place taxpayer funds in a range of options available to them today. SB 553 proposes changes to taxpayer funds once they are placed within PDIP.

Collateralization of funds is commonplace in municipalities and states throughout the country as a way of providing additional protectional and security of taxpayer funds.

Some states with such requirements include:

- Louisiana

- New Jersey

- Mississippi

- Oregon

- Texas

There are $50 billion in bank deposits held by banks in New Hampshire and they are able to support the increased deposit inflows. All of current PDIP funds would represent a overall increase of the collective bank's deposit base of 1%.

The legislation makes changes to the operation of PDIP beginning on June 22, 2025 after the contract with the current fund manager expires. It is too soon to know what entities will want to manage the funds as laid out in SB 553.

The State was already scheduled to issue a request for proposal for the next PDIP contract to manage the funds. Once that happens, we will learn more about which organizations want to manage the taxpayer funds held in PDIP.

Join SB553 Supporters Today

SB553 passed the NH Senate with a vote of 24-0.

In addition to the bi-partisan legislators co-sponsoring the bill, bankers throughout New Hampshire's banking industry, their board members, members of the public, chambers of commerce and economic development groups are all supporting this commonsense legislation to help grow our economy, increase access to credit for small businesses, and keep our funds local.

Join the supporters today and help us pass this bill in the House of Representatives by sending an email rhale@nhbankers.com

Supporters of SB553:

- Bankers throughout New Hampshire, their board members and members of the public

- Business and Industry Association of New Hampshire

- Belknap Economic Development Council

- Eric Chinburg, President of Chinburg Properties

- Steve Duprey, President at Foxfire Property Management and The Duprey Companies

- Several Chambers of Commerce: Greater Concord, Greater Dover, Greater Manchester, Greater Nashua, Lakes Region and Mt. Washington Valley, Upper Valley Business Alliance

- NH Auto Dealers Association